Model Combination in Risk Sharing under Ambiguity

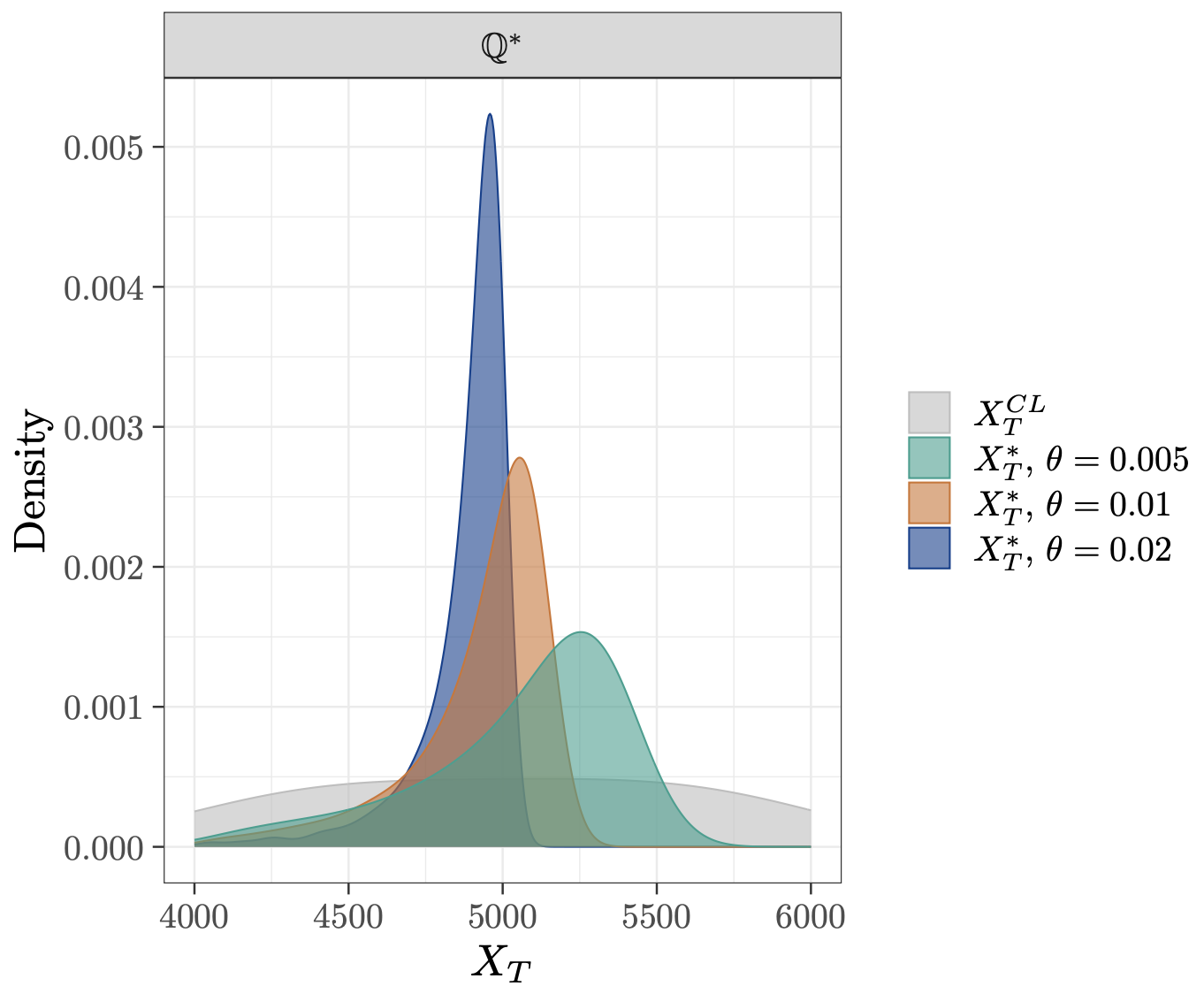

We consider the problem of an agent who faces losses over a finite time horizon and may choose to share some of these losses with a counterparty. The agent is uncertain about the true loss distribution and has multiple models for the losses. Their goal is to optimize a mean-variance type criterion with model combination under ambiguity through risk sharing.