Actuarial Research Conference 2025

Last week, I presented on my recent preprint ‘Model Ambiguity in Risk Sharing with Monotone Mean-Variance’ at the 60th Actuarial Research Conference, which was held at York University.

Last week, I presented on my recent preprint ‘Model Ambiguity in Risk Sharing with Monotone Mean-Variance’ at the 60th Actuarial Research Conference, which was held at York University.

I’m happy to share that yesterday I successfully defended my thesis “Model ambiguity in continuous time non-life insurance” at the University of Toronto.

I’m excited to share that our paper Optimal robust reinsurance with multiple insurers has been published online in Scandinavian Actuarial Journal. This is joint work with Sebastian Jaimungal and Silvana Pesenti.

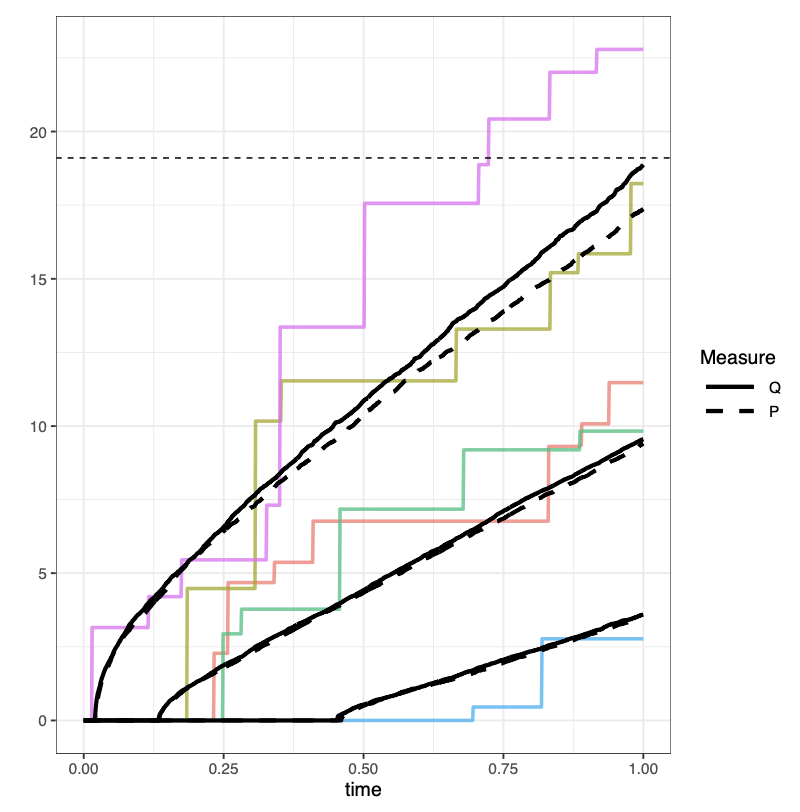

I’m excited to share that the first paper from my PhD, Stressing dynamic loss models, has been published this month in Insurance: Mathematics and Economics. In this paper, we applied a reverse stress testing approach to compound Poisson loss models. This is joint work with my PhD supervisors Sebastian Jaimungal and Silvana Pesenti.

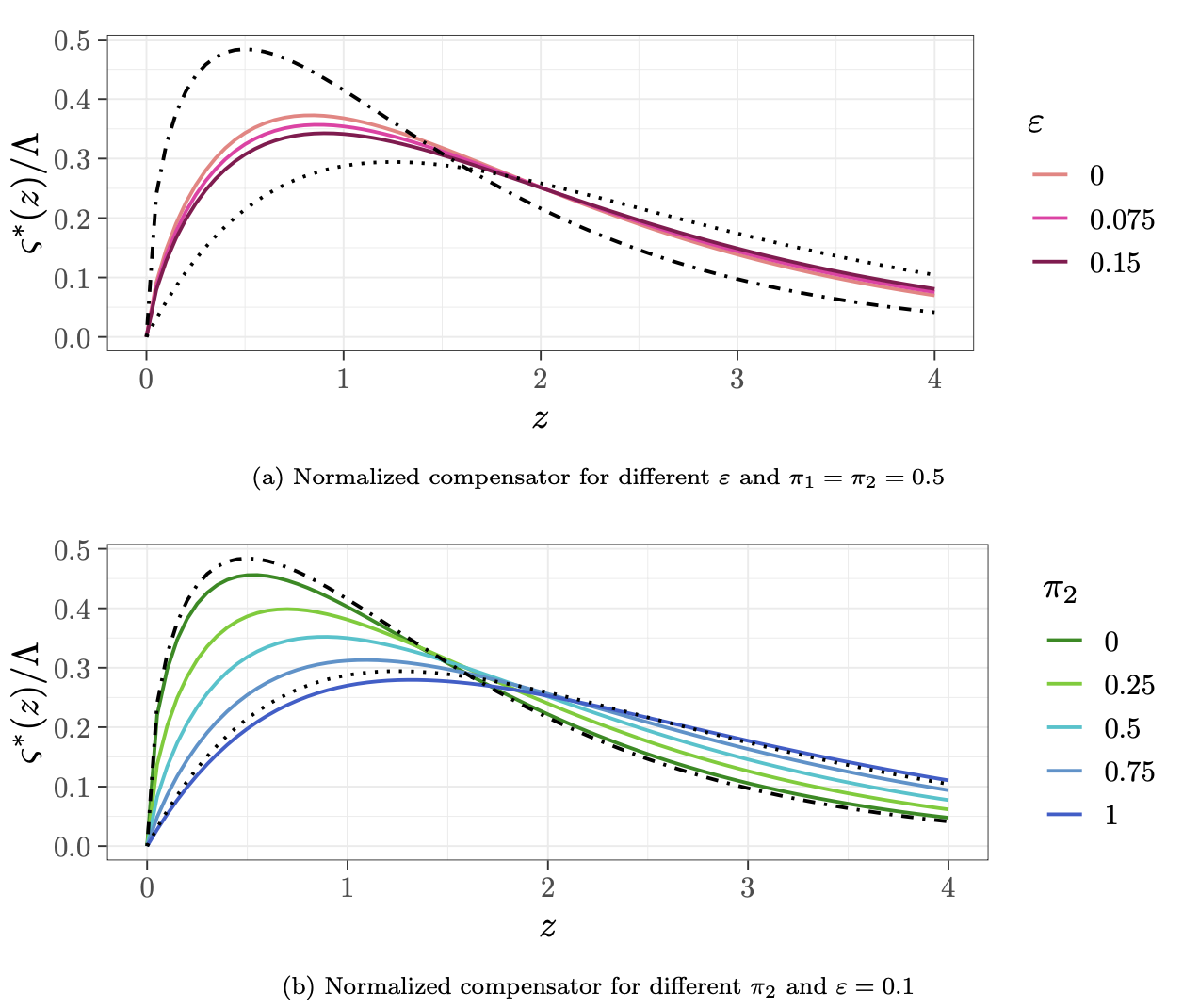

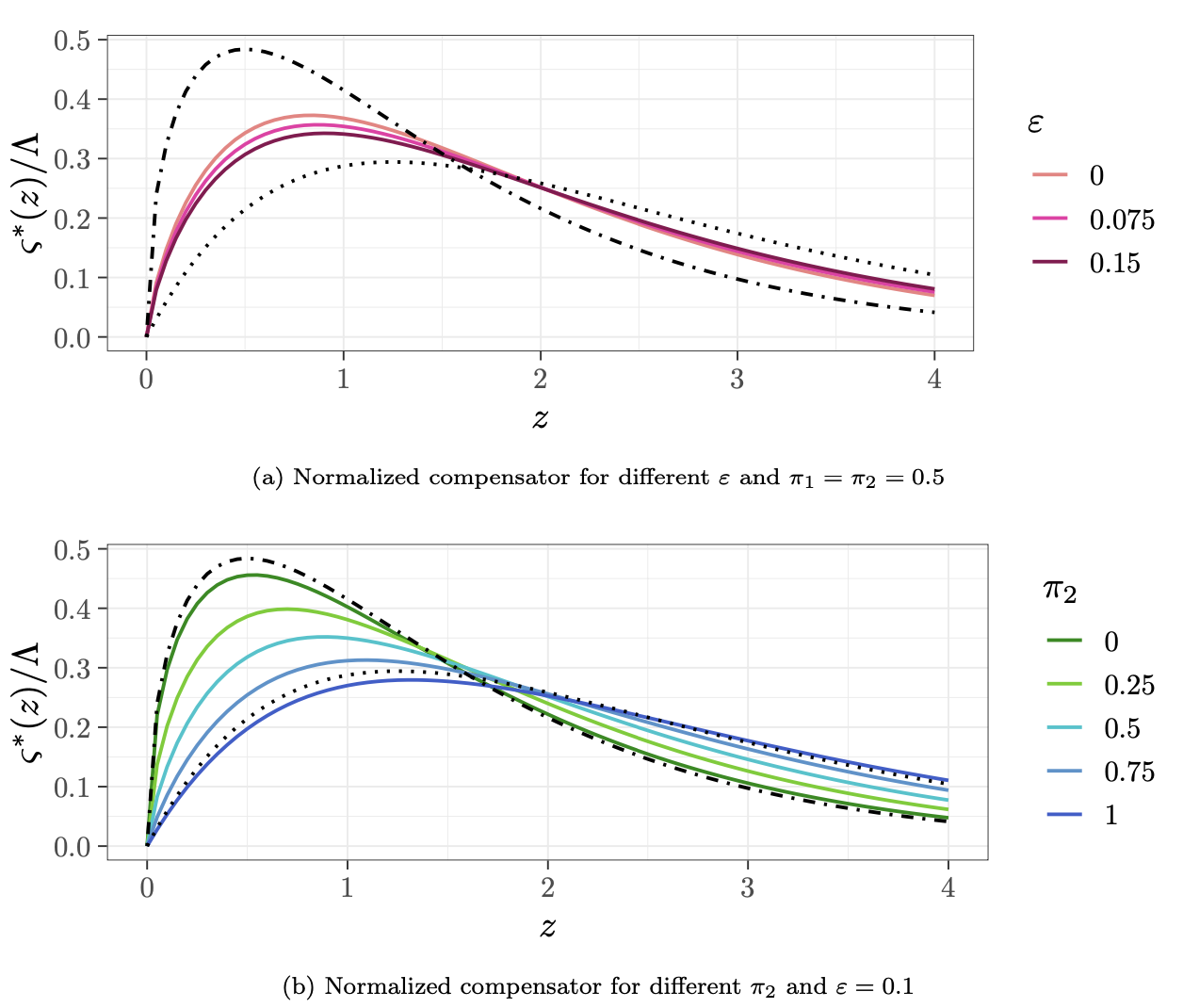

I’m excited to share that my most recent doctoral work is now available as a pre-print. In this paper, we explore the problem of an ambiguity-averse reinsurer who prices reinsurance contracts for different insurance companies. The insurers have different beliefs about the underlying loss model, and the reinsurer must determine which model to price under given this.